What This Document Is

This resource is a detailed solution set for a practice problem focused on foundational accounting principles. Specifically, it addresses concepts covered in Chapter Three of Principles of Financial Accounting (ACCT 2610) at Washington University in St. Louis. It’s designed to reinforce understanding of how transactions impact key financial statement accounts and the accounting equation. The practice problem likely involves a scenario requiring the application of debit and credit rules, and the preparation of a trial balance or similar summary.

Why This Document Matters

Students enrolled in ACCT 2610 will find this particularly helpful when reviewing practice problems and solidifying their grasp of core accounting mechanics. It’s ideal for use *after* attempting the practice problem independently – comparing your approach to a fully worked solution is a powerful learning technique. This resource is most beneficial when you’re looking to identify areas where your understanding needs strengthening, or when you want to confirm you’re applying accounting principles correctly. It’s a valuable tool for exam preparation and building confidence in your problem-solving abilities.

Common Limitations or Challenges

This solution set does *not* provide step-by-step instructions on *how* to arrive at the answers. It assumes you’ve already engaged with the problem and are seeking to evaluate your work. It won’t explain the underlying accounting concepts themselves; it’s built for application, not initial learning. Furthermore, it focuses solely on this specific practice problem and won’t cover all possible accounting scenarios. Accessing the full solution set requires a purchase.

What This Document Provides

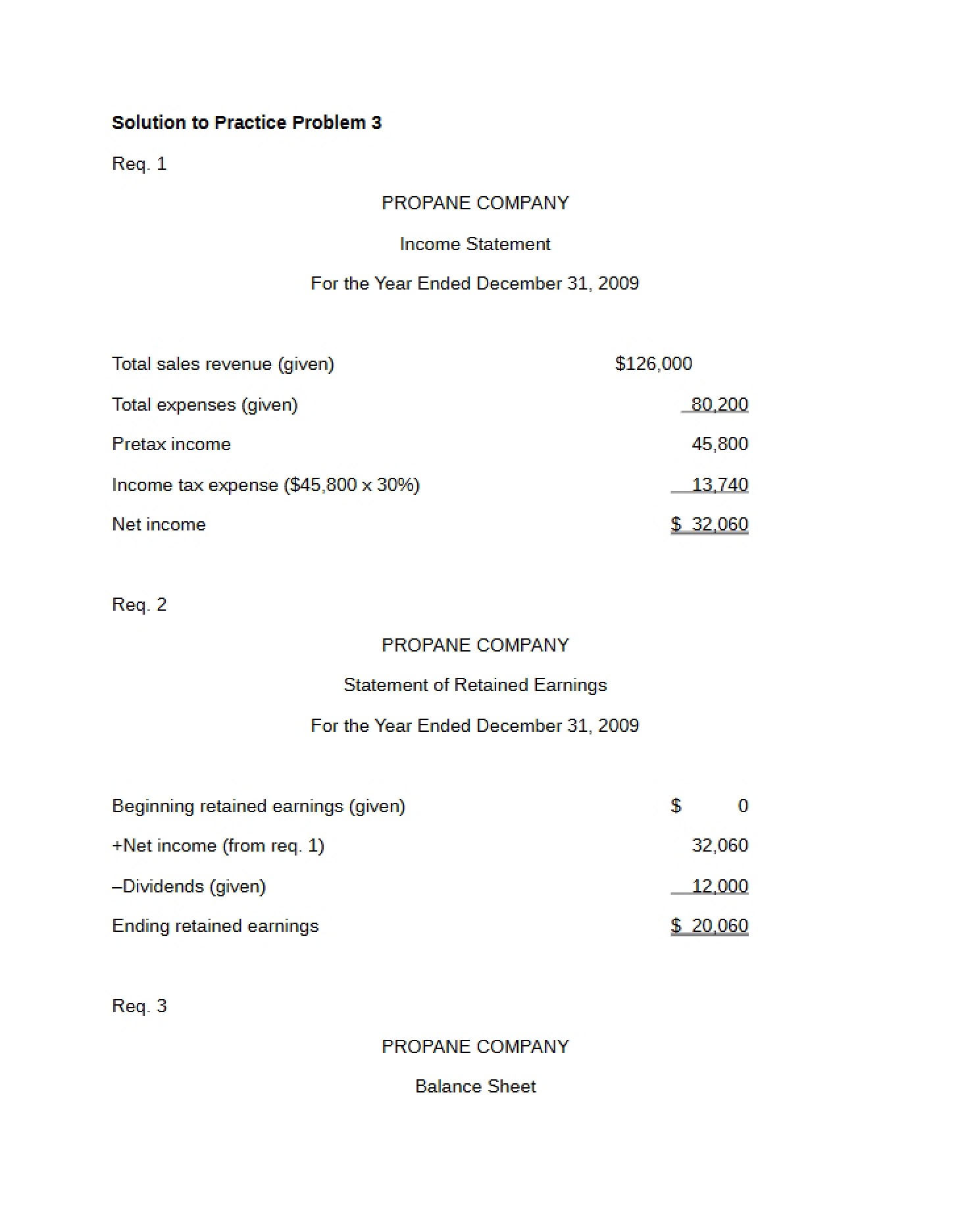

* A complete listing of account balances, categorized by asset, liability, and equity accounts.

* Detailed figures relating to revenue-generating activities, such as catering and food sales.

* Breakdowns of various expense accounts, including costs related to food, utilities, and wages.

* Information pertaining to long-term assets like buildings and equipment.

* Account balances for notes payable and mortgage payable, representing financing obligations.

* A clear presentation of beginning balances and changes to retained earnings.