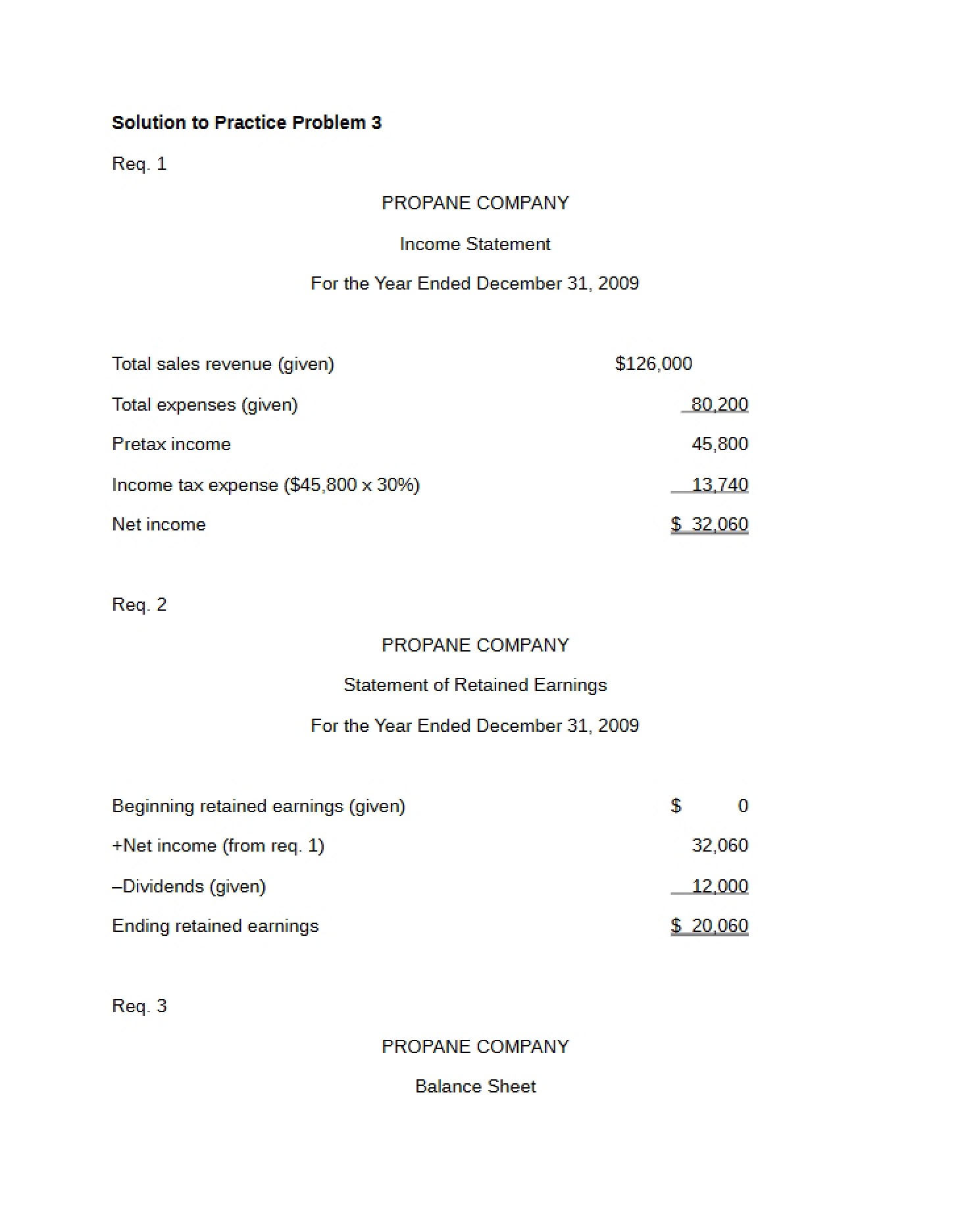

What This Document Is

This resource is a detailed illustration of a core financial accounting principle: the Statement of Cash Flows. It focuses on a specific company, Bauer Company, and presents a complete example of how to categorize and report cash inflows and outflows. The statement is prepared using the indirect method, a common technique for deriving cash flow from operating activities. This example covers all three primary sections of the statement – operating, investing, and financing activities – providing a comprehensive view of a company’s liquidity position over a reporting period.

Why This Document Matters

Students enrolled in Principles of Financial Accounting (ACCT 2610) at Washington University in St. Louis will find this particularly helpful when learning to prepare and analyze cash flow statements. It’s ideal for reinforcing understanding after lectures and textbook readings, and can be used as a reference while working through homework assignments or preparing for assessments. Individuals struggling to differentiate between the three activity types or understand the impact of various balance sheet changes on cash flow will benefit greatly from studying this example. It’s a valuable tool for solidifying your grasp of a fundamental accounting concept.

Common Limitations or Challenges

While this resource provides a complete example, it does *not* offer step-by-step instructions on *how* to create a Statement of Cash Flows from raw data. It also doesn’t include explanations of the underlying accounting principles for each transaction. It’s designed to be a demonstrative example, not a teaching tutorial. Furthermore, it focuses solely on the indirect method; the direct method is not covered. It’s important to remember that this is a single company example and may not encompass all possible scenarios.

What This Document Provides

* A fully prepared Statement of Cash Flows for Bauer Company, dated December 31, 2004.

* Categorization of cash flows into operating, investing, and financing activities.

* Illustrative adjustments to net income to arrive at cash flow from operations.

* Presentation of non-cash investing and financing activities.

* Calculation of the net increase in cash and the resulting ending cash balance.

* A clear depiction of how changes in various balance sheet accounts impact cash flow.