What This Document Is

This study guide provides a focused review of key concepts within the accounting cycle, specifically building upon foundational principles covered in a Principles of Financial Accounting course (ACCT 2610) at Washington University in St. Louis. It delves into the processes that occur *during* and *at the end* of an accounting period, offering a detailed look at how financial information is prepared and summarized. This material represents Part Two of Chapter Four notes, likely covering topics discussed in Class 7.

Why This Document Matters

Students enrolled in introductory financial accounting courses will find this resource particularly helpful. It’s ideal for reinforcing lecture material, preparing for quizzes and exams, and solidifying understanding of the steps involved in creating accurate financial statements. Those struggling with the flow of the accounting cycle, or needing a clear explanation of the ‘why’ behind adjusting and closing entries, will benefit most. It’s best used *after* initial exposure to the concepts in class and alongside textbook readings.

Common Limitations or Challenges

This resource is designed as a supplemental study aid and does not replace the need for comprehensive textbook study or active participation in class. It does not include practice problems or detailed worked examples. It focuses on the conceptual framework and process flow, and won’t provide complete solutions to accounting challenges. It assumes a basic understanding of fundamental accounting terminology and principles.

What This Document Provides

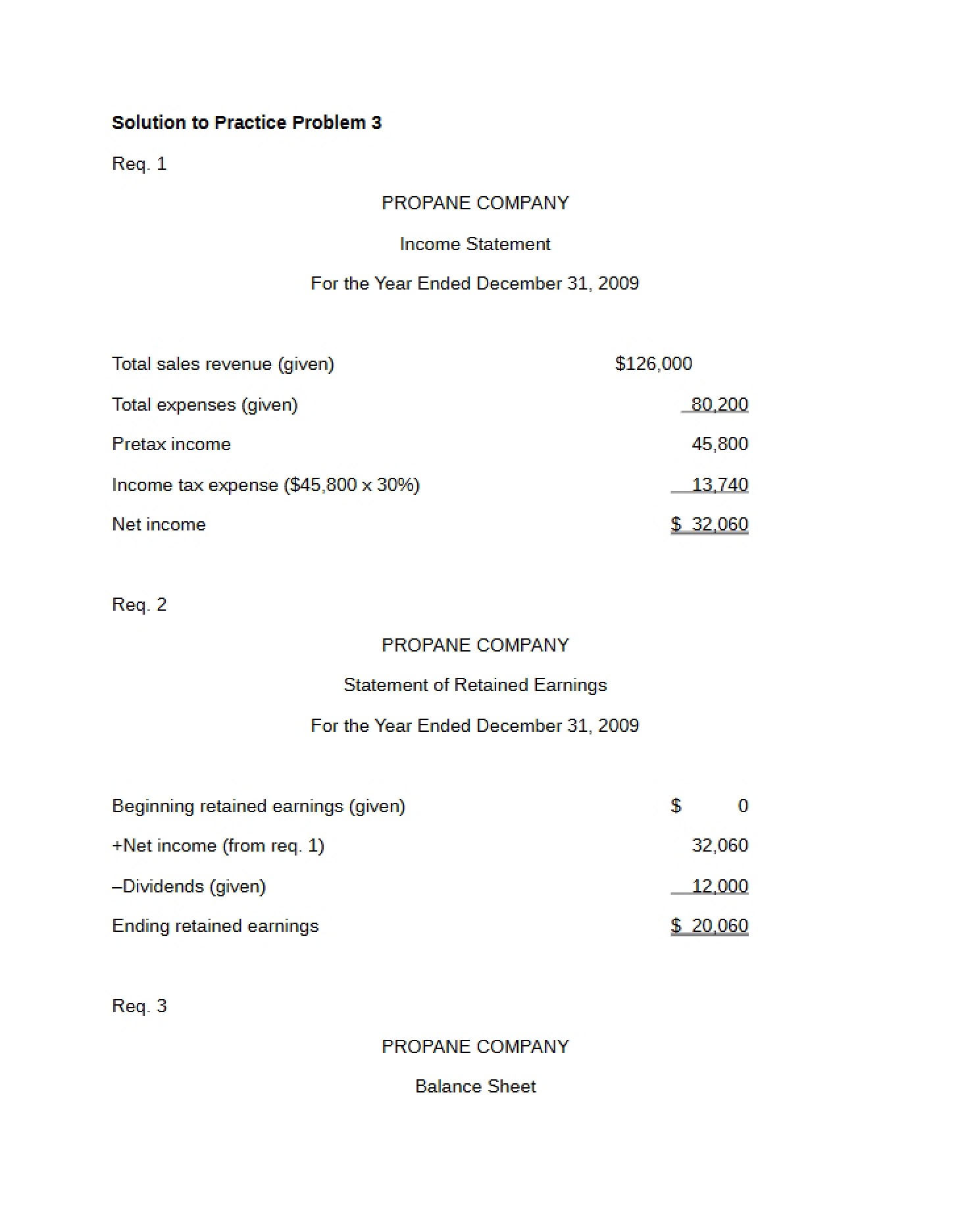

* A structured overview of the phases within the accounting cycle.

* An explanation of the purpose and necessity of the adjustment process.

* Discussion of the distinctions between temporary and permanent accounts.

* An outline of the steps involved in the closing process.

* Illustrative examples of trial balance formats.

* Consideration of how financial statements are interconnected.

* A preview of topics related to preparing a post-closing trial balance.