What This Document Is

This study guide provides a focused overview of key concepts covered in Chapter Six of ACCT 2610: Principles of Financial Accounting at Washington University in St. Louis. It centers around the critical accounting processes related to revenue recognition and the management of accounts receivable. This resource is designed to help students solidify their understanding of how and when companies record revenue, and how they account for potential uncollectible amounts from customers.

Why This Document Matters

Students enrolled in ACCT 2610 will find this guide particularly helpful when preparing for quizzes and exams related to the revenue cycle and balance sheet accounts. It’s ideal for reinforcing lecture material and building a strong foundation for more advanced accounting topics. Those struggling with the timing of revenue recognition, or the complexities of dealing with customer credit and potential bad debts, will benefit most from a detailed review of the concepts presented. Use this as a companion to your textbook and class notes to maximize comprehension.

Common Limitations or Challenges

This guide is a summary and does *not* include detailed practice problems or worked examples. It will not substitute for completing assigned homework or actively participating in class. The guide focuses on conceptual understanding and does not provide comprehensive coverage of all possible scenarios or industry-specific applications. It assumes a basic understanding of the accounting equation and fundamental journal entry principles.

What This Document Provides

* An overview of the principles governing revenue recognition, including considerations for shipping terms.

* A breakdown of the components used in calculating net sales figures.

* Discussion of methods for recording transactions involving sales discounts.

* An exploration of profit margin analysis techniques.

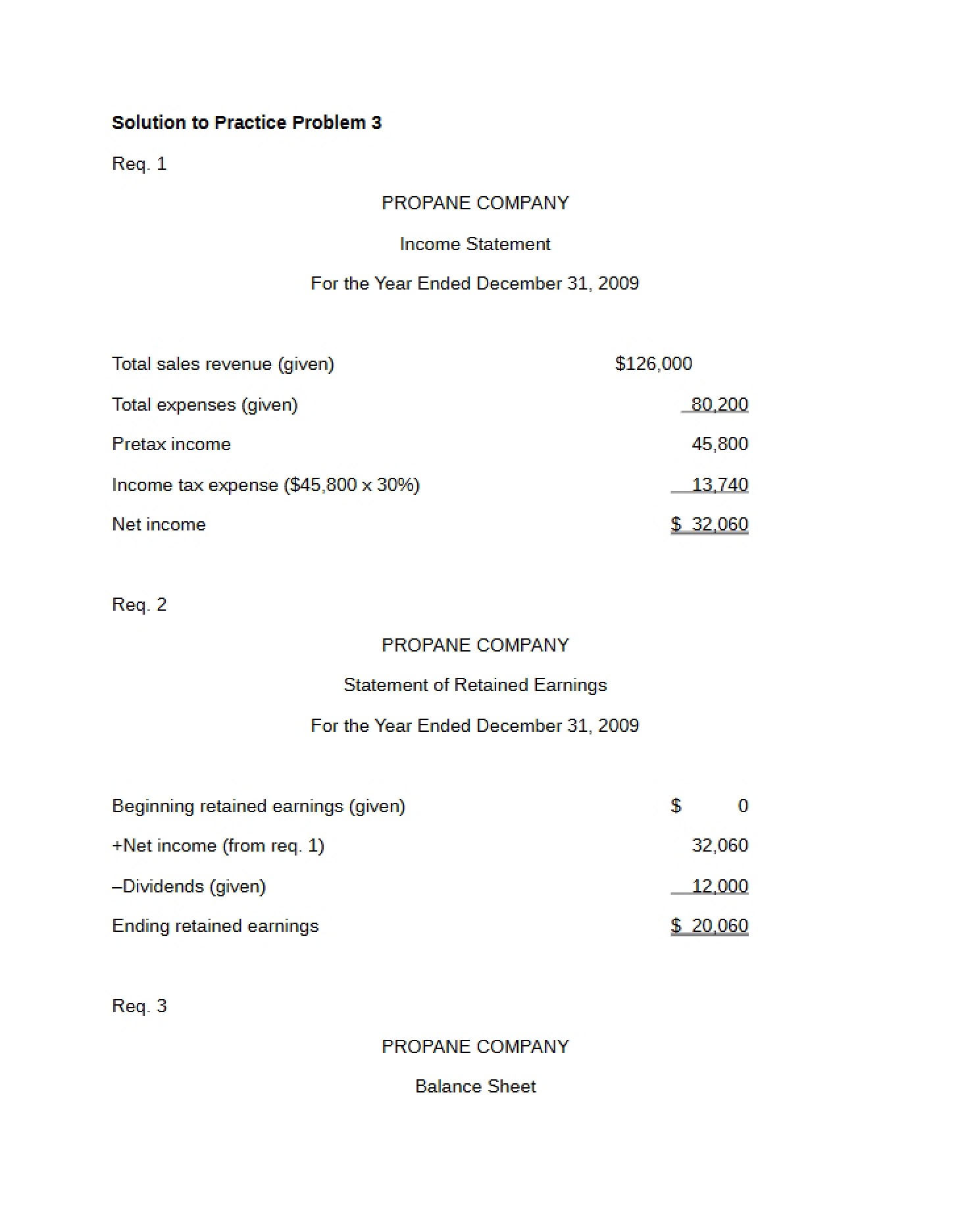

* A detailed look at accounting for bad debts, including required and alternative methods.

* Guidance on estimating bad debt expense using different approaches.

* Explanation of how accounts receivable are reported on the balance sheet.