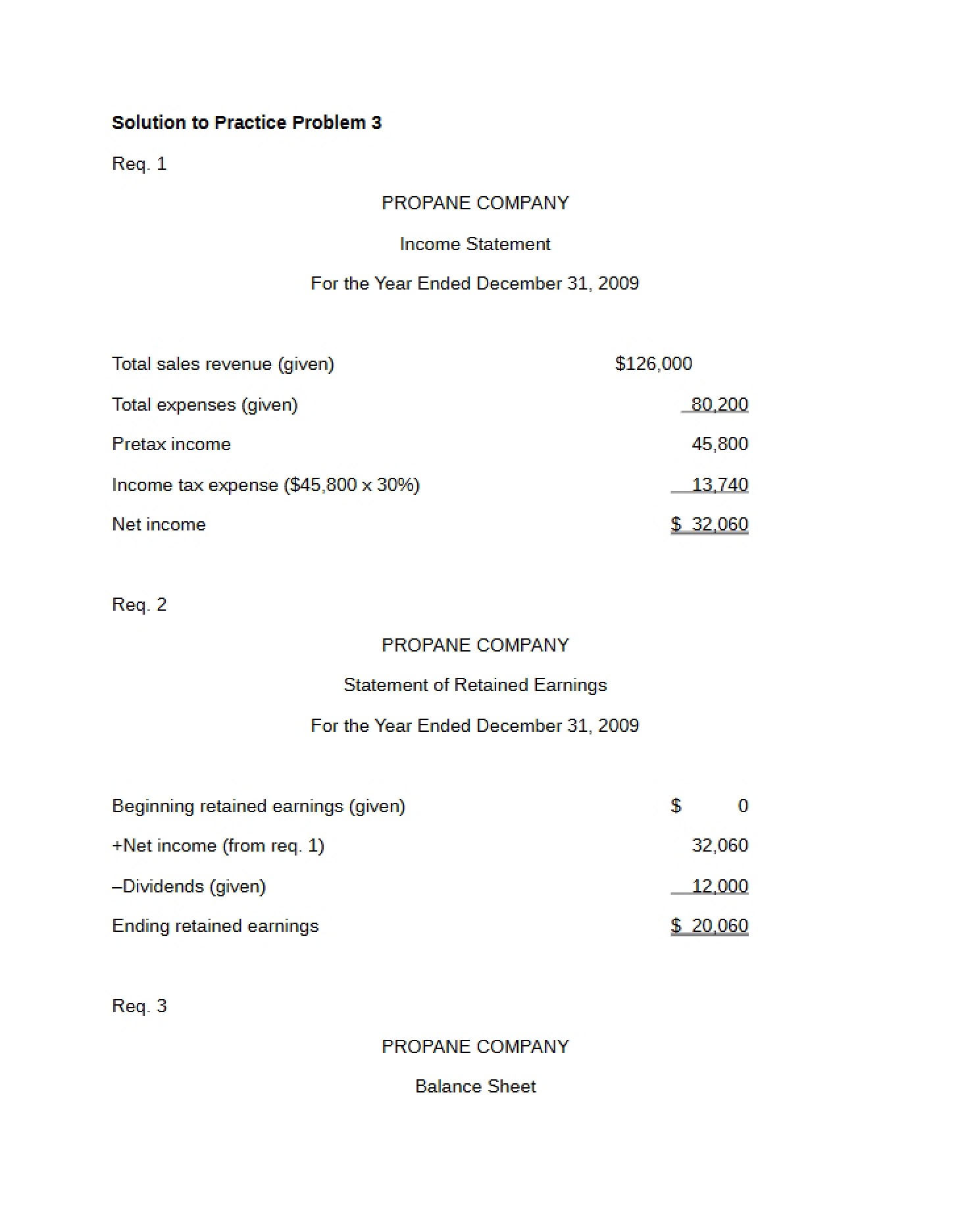

What This Document Is

This resource is a focused summary centered around the Statement of Cash Flows, a core component of financial accounting. Specifically, it delves into the practical application of the *indirect method* for constructing this vital financial statement. It presents the typical structure and categorization used when reporting cash activities, offering a detailed look at how different financial elements contribute to the overall cash position of a company. The summary also touches upon the *direct method* as a point of comparison.

Why This Document Matters

Students enrolled in Principles of Financial Accounting (like ACCT 2610 at Washington University in St. Louis) will find this particularly useful when mastering the intricacies of cash flow statement preparation. It’s ideal for reinforcing understanding *after* initial lectures and textbook readings, and serves as a strong foundation for tackling related homework assignments and exam questions. Anyone preparing to analyze a company’s financial health will benefit from a firm grasp of the concepts presented here, as the Statement of Cash Flows provides crucial insights into a company’s liquidity and financial flexibility.

Common Limitations or Challenges

This summary provides a structural overview and conceptual framework. It does *not* include detailed, step-by-step instructions for calculating each line item, nor does it offer worked examples demonstrating the application of these principles to specific scenarios. It also doesn’t cover advanced topics like the statement of cash flows under IFRS standards, or detailed analyses of cash flow patterns. Access to the full resource is required for a complete understanding of the calculations and nuances involved.

What This Document Provides

* A clear presentation of the standard format for a Statement of Cash Flows using the indirect method.

* Categorization of cash flow activities into Operating, Investing, and Financing sections.

* Identification of common adjustments made to net income when using the indirect method.

* Overview of typical items included within each cash flow category (e.g., purchases of fixed assets, proceeds from sale of shares).

* A comparative look at the direct method of presenting cash flows from operating activities.

* Notes on common expense classifications within operating activities.