What This Document Is

This is a practice midterm exam for ACCT 2610, Principles of Financial Accounting, at Washington University in St. Louis. Specifically, it represents the second midterm assessment from the Fall 2007 semester. It’s designed to test your understanding of intermediate-level accounting concepts covered in the course up to that point in the semester. The format mirrors a typical in-class exam, including a time limit and closed-book conditions.

Why This Document Matters

This resource is invaluable for students currently enrolled in or preparing for Principles of Financial Accounting. It’s particularly useful for assessing your preparedness for mid-term examinations. Working through practice problems helps solidify your understanding of key concepts, identify areas where you need further study, and become comfortable with the exam format and question types used by Professor Martin. It’s best utilized *after* you’ve completed the relevant readings and classwork, as a way to gauge your mastery of the material.

Common Limitations or Challenges

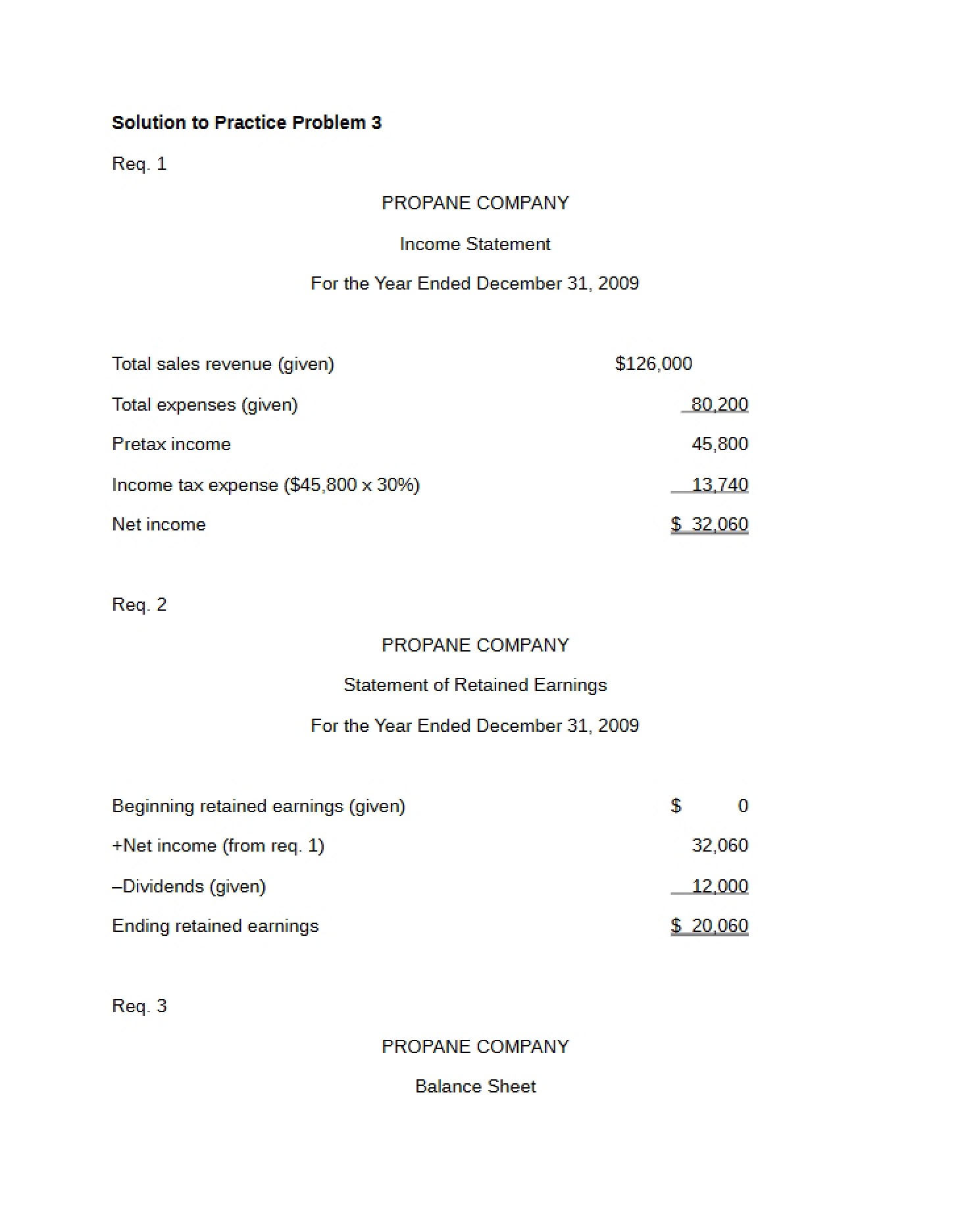

This document is a *practice* exam, and therefore does not represent a comprehensive review of *all* possible topics covered in the course. It focuses on a specific set of concepts as they were emphasized during the Fall 2007 semester. It does not include detailed explanations of the correct answers or step-by-step solutions – it’s designed to challenge you to apply your knowledge independently. Access to the full document is required to view the complete questions and assess your performance.

What This Document Provides

* A range of multiple-choice questions testing core accounting principles.

* Problem-solving scenarios involving asset depreciation methods (straight-line and double-declining balance).

* Questions relating to liability recognition, including contingent and deferred tax liabilities.

* A complex case study involving multiple assets (machine and truck) requiring calculations of depreciation expense and potential gains/losses on disposal.

* An excerpt from a company’s financial statement footnote regarding accounts receivable and allowance for doubtful accounts.

* A clear indication of point values assigned to each question, allowing for strategic time management during exam practice.