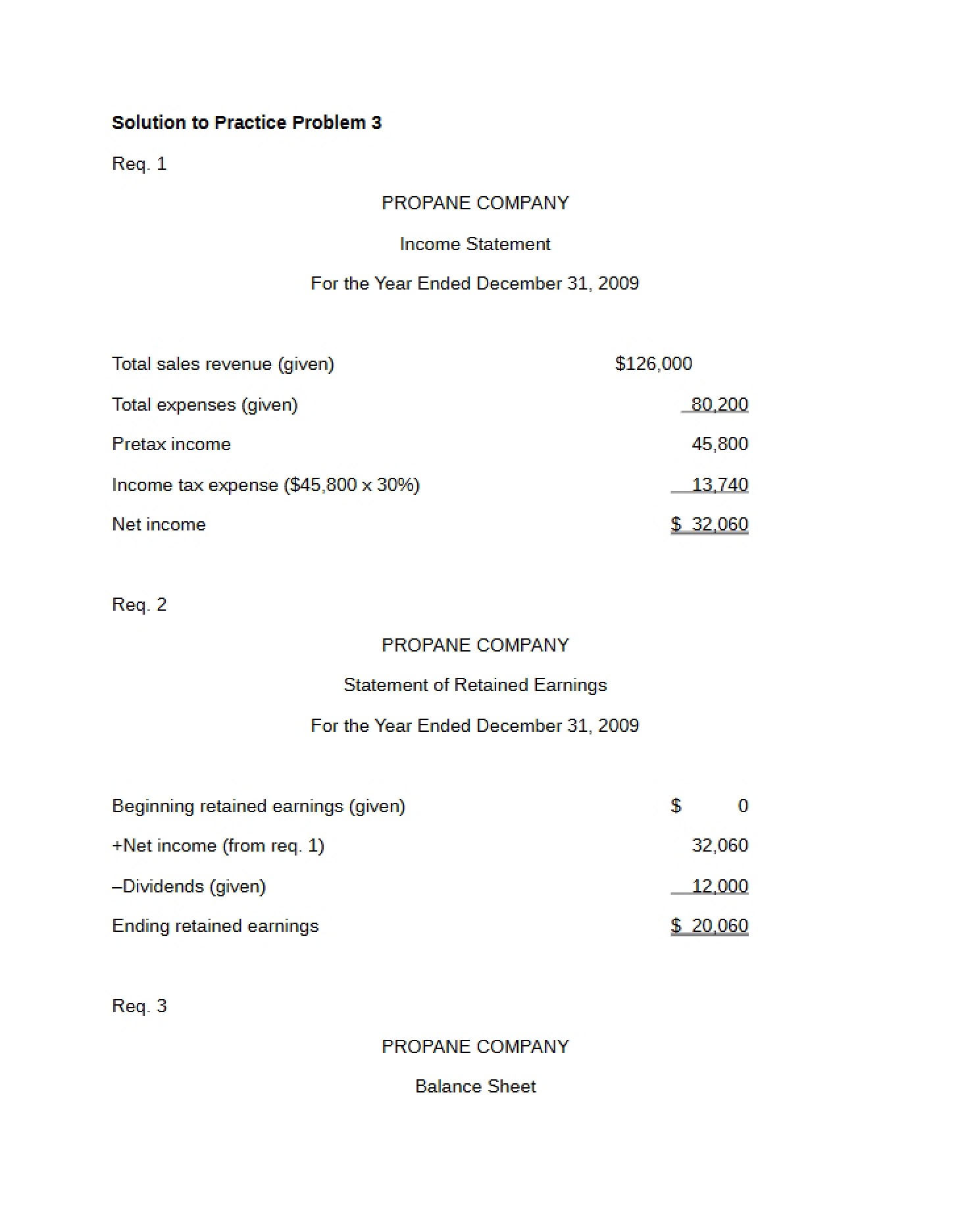

What This Document Is

This resource presents a detailed solution for a practice problem (PP2) focused on the preparation and analysis of the Statement of Cash Flows for the fictional Leonard Company. It’s designed for students learning the intricacies of financial accounting, specifically how to categorize and report cash inflows and outflows. The solution demonstrates application of both the indirect and direct methods for calculating cash flow from operations, alongside analyses of investing and financing activities. This is a worked example intended to solidify understanding of core accounting principles.

Why This Document Matters

Students enrolled in introductory financial accounting courses – like ACCT 2610 at Washington University in St. Louis – will find this particularly helpful. It’s ideal for those working through similar practice problems as part of their coursework or preparing for quizzes and exams. If you’re struggling to correctly classify transactions into operating, investing, and financing activities, or are unsure how to reconcile net income to cash flow, this solution can serve as a valuable reference. It’s best used *after* attempting the problem independently to maximize learning.

Common Limitations or Challenges

This solution focuses specifically on Leonard Company’s cash flow statement for the year 2001. It does *not* provide a comprehensive explanation of the underlying accounting principles for cash flows; rather, it assumes a foundational understanding of these concepts. It also doesn’t offer alternative approaches to problem-solving or address more complex scenarios involving multiple currencies or non-cash investing/financing activities. It is a single example and shouldn’t be considered a substitute for a thorough understanding of the course material.

What This Document Provides

* A complete Statement of Cash Flows prepared using the indirect method.

* A separate presentation of Cash Flows from Operations calculated using the direct method.

* Detailed categorization of various transactions into operating, investing, and financing activities.

* Illustrative figures demonstrating the impact of items like depreciation, gains/losses on asset sales, and changes in working capital accounts on cash flow.

* A clear presentation of the calculation of the net increase (or decrease) in cash balance.

* Beginning and ending cash balance figures for the period.