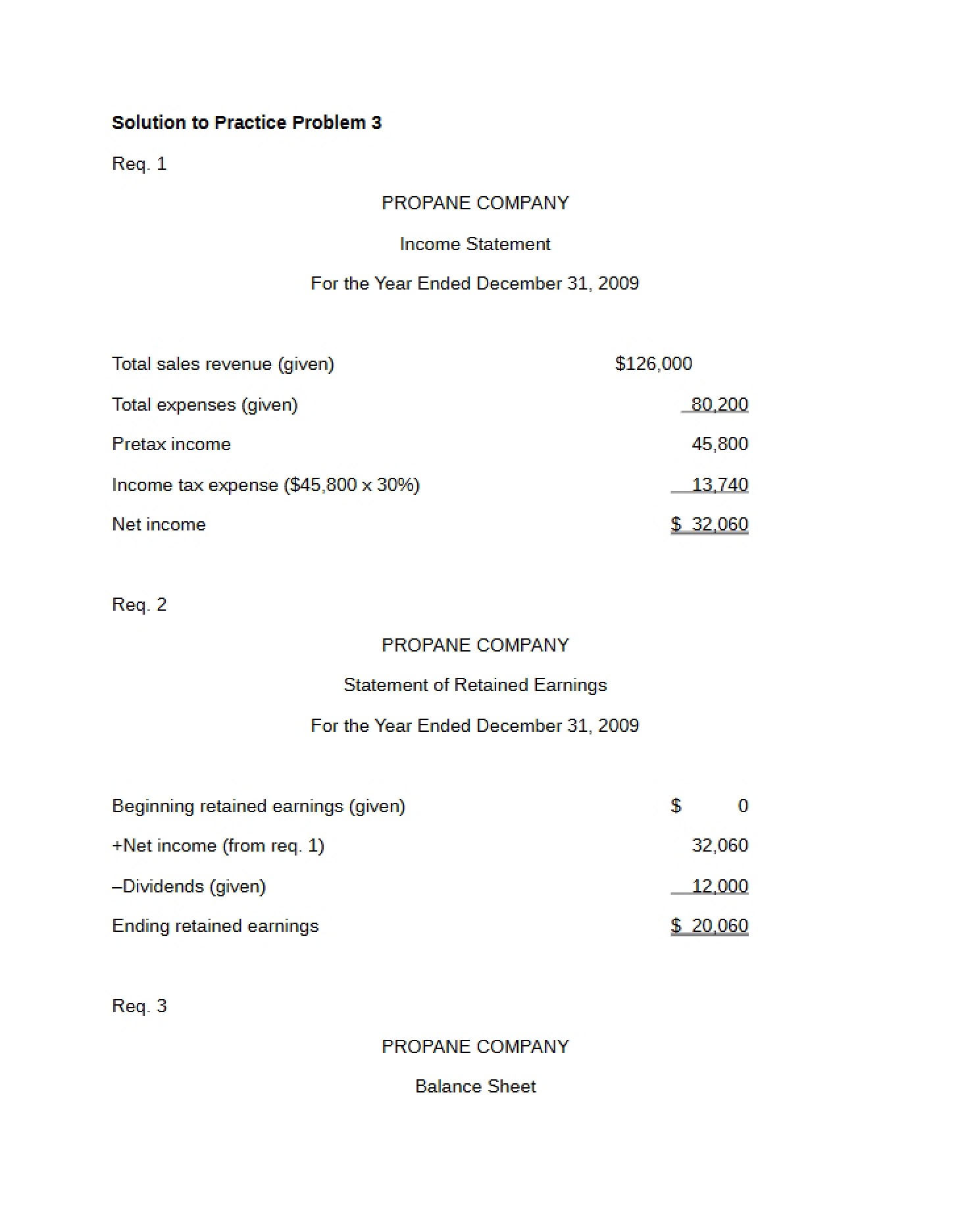

What This Document Is

This resource is a detailed solution set for a practice problem focused on core principles within introductory financial accounting. Specifically, it addresses the application of accrual accounting concepts, diving into the recognition of revenues and expenses. The practice problem centers around scenarios requiring adjustments to ensure financial statements accurately reflect a company’s financial performance and position. It’s designed to reinforce understanding of key accounting adjustments made *before* preparing formal financial statements.

Why This Document Matters

Students enrolled in Principles of Financial Accounting (like ACCT 2610 at Washington University in St. Louis) will find this particularly helpful when working through assigned practice problems or preparing for assessments. It’s ideal for those who need to solidify their understanding of when and how to record deferrals and accruals. This is a crucial step in mastering the fundamentals, as these concepts form the basis for more advanced accounting topics. If you’re struggling to apply the matching principle or understand the timing of revenue and expense recognition, this solution set can provide valuable insight – *after* you’ve attempted the problem yourself.

Common Limitations or Challenges

This resource focuses *solely* on the solution to a single practice problem. It does not offer comprehensive explanations of the underlying accounting principles themselves. It assumes you have already been introduced to concepts like deferred revenue, accrued expenses, and depreciation. Furthermore, it doesn’t provide alternative approaches to solving the problem or address more complex scenarios beyond the scope of the initial practice question. It is not a substitute for attending lectures, reading the textbook, or seeking clarification from your instructor.

What This Document Provides

* A detailed breakdown of journal entries related to common accrual adjustments.

* Illustrations of how to apply accounting principles to real-world business scenarios.

* Examples of adjustments for items such as unearned revenue, accrued revenue, prepaid expenses, and accrued expenses.

* Application of depreciation calculations and related journal entries.

* Demonstration of how to account for items like property taxes and interest.

* A structured format for analyzing and resolving accounting adjustment problems.