What This Document Is

This resource is a detailed solution walkthrough for a practice problem set within the Principles of Financial Accounting (ACCT 2610) course at Washington University in St. Louis. Specifically, it focuses on applying foundational accounting principles to a series of scenarios. It’s designed to reinforce understanding of core concepts covered in Chapter 2 and prepare students for more complex assessments. The practice problems likely involve the preparation and analysis of financial statements, and the application of accounting equations.

Why This Document Matters

Students enrolled in ACCT 2610 will find this particularly helpful when reviewing challenging practice problems. It’s ideal for use *after* attempting the problems independently – allowing you to check your work and identify areas where your understanding needs strengthening. This resource is best utilized during study sessions, as a supplement to lectures, or when preparing for quizzes and exams. It’s a valuable tool for solidifying your grasp of fundamental accounting techniques and building confidence in your problem-solving abilities.

Common Limitations or Challenges

This solution set does *not* provide step-by-step instructions on *how* to approach the problems. It assumes you have already attempted the problems and are looking for a comparison to your own work. It will not explain the underlying accounting principles themselves; rather, it demonstrates their application in specific contexts. It also doesn’t offer alternative solution methods or detailed explanations of why certain approaches are preferred. Access to the original practice problem set is required to fully benefit from this resource.

What This Document Provides

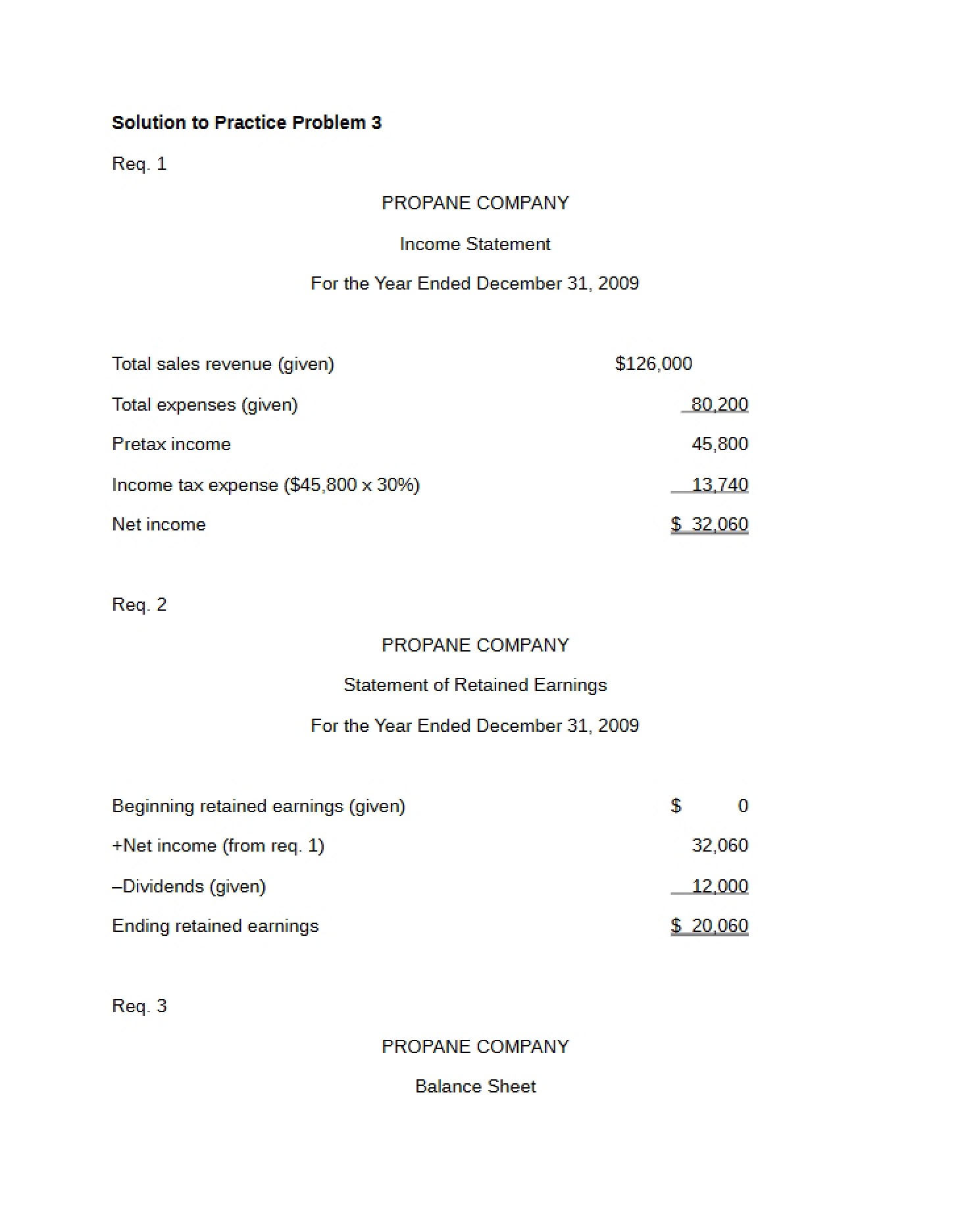

* A comprehensive overview of solutions related to short-term and long-term asset and liability accounts.

* Illustrative examples demonstrating the impact of various transactions on account balances.

* Detailed presentations of account schedules, likely including beginning and ending balances.

* Information relating to the statement of retained earnings and contributed capital.

* A framework for understanding how different accounting elements interact within a broader financial context.