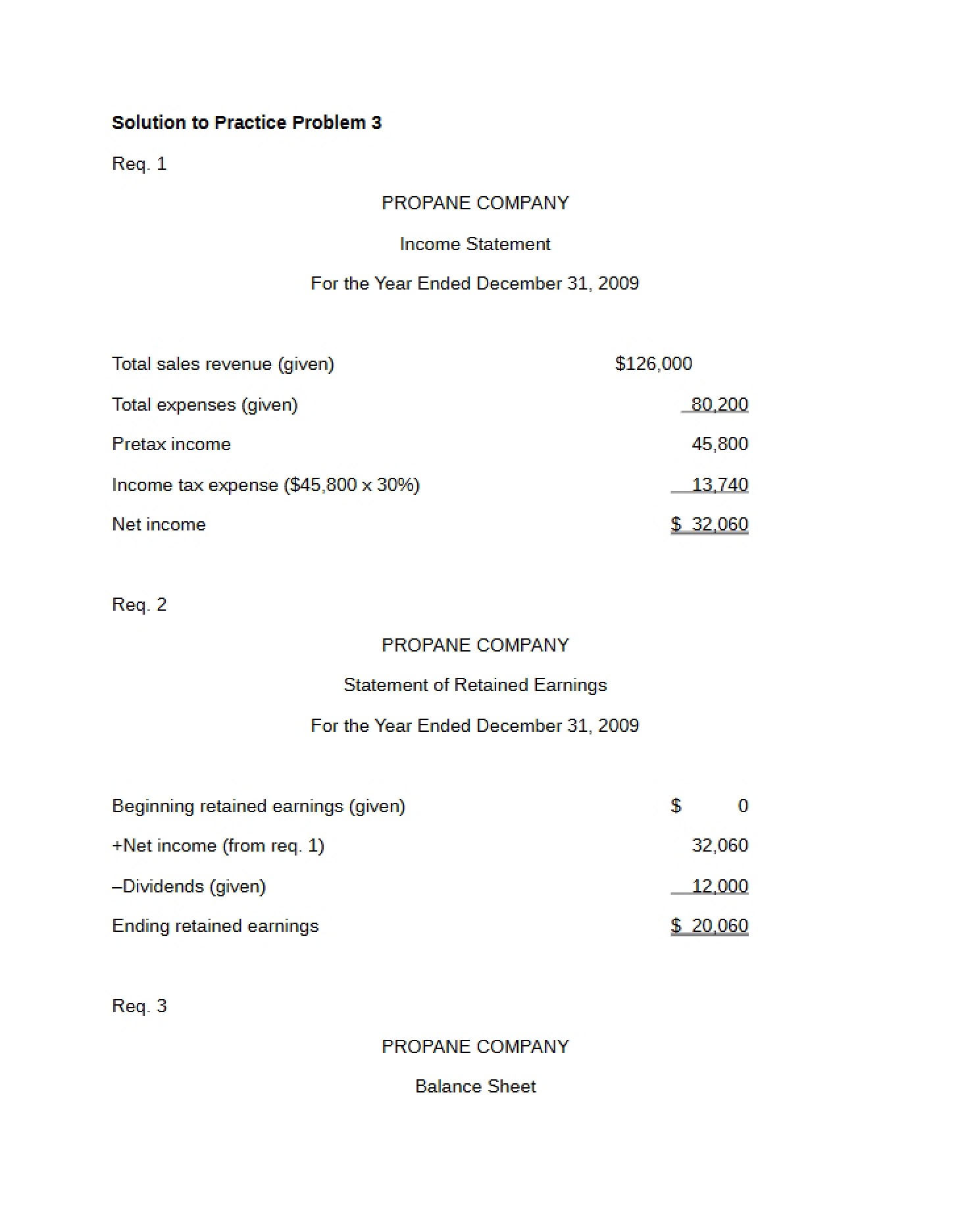

What This Document Is

This document is a past quiz from Principles of Financial Accounting (ACCT 2610) at Washington University in St. Louis, originally administered in Spring 2008. It’s designed to assess understanding of key accounting principles covered in the course, focusing on topics related to asset valuation, depreciation methods, and the accounting treatment of specific transactions. The quiz format includes both short-answer problems requiring calculations and conceptual questions testing qualitative understanding.

Why This Document Matters

Students currently enrolled in or preparing for similar financial accounting courses will find this resource particularly valuable. It provides a realistic example of the types of questions and challenges presented in a university-level accounting assessment. Utilizing past quizzes like this one is an excellent way to test your knowledge, identify areas where further study is needed, and familiarize yourself with the instructor’s expectations. It’s especially helpful for students preparing for midterms or final exams, or those seeking to reinforce their understanding of core concepts.

Common Limitations or Challenges

Please be aware that this is a past assessment and may not perfectly reflect the exact content or weighting of current evaluations. Accounting standards and interpretations can evolve, so while the fundamental principles remain relevant, specific applications might differ. This resource does *not* include detailed explanations or solutions; it’s intended as a practice tool to gauge your existing knowledge, not as a substitute for thorough study and understanding of course materials.

What This Document Provides

* Problems relating to depreciation calculations using methods like Double-Declining Balance.

* Scenarios involving the sale of assets and the necessary journal entries to record those transactions.

* Conceptual questions regarding the appropriate accounting treatment for specific items, such as gifts or donations.

* Questions testing understanding of how changes in accounting estimates are handled under U.S. GAAP.

* A true/false statement assessing knowledge of accelerated depreciation methods compared to straight-line depreciation.