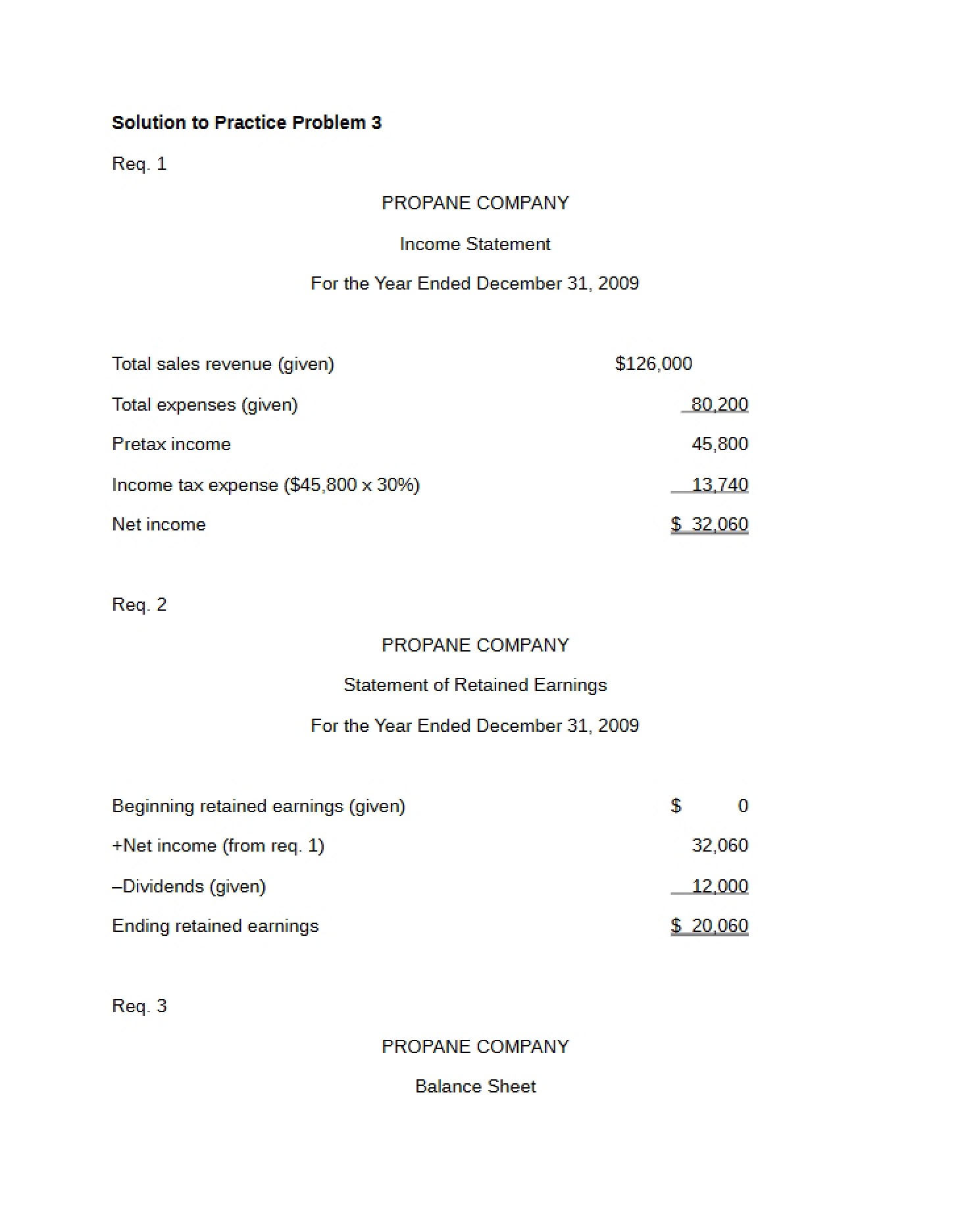

What This Document Is

This resource is a detailed example illustrating the preparation of a Statement of Cash Flows, a core component of a company’s financial statements. It focuses on a specific business, “Later Gator Lounge,” and demonstrates how to categorize and present cash inflows and outflows. The example showcases two common methods for calculating cash flow from operations: the direct method and the indirect method. It’s designed to complement your understanding of ACCT 2610 principles related to cash flow analysis.

Why This Document Matters

Students enrolled in Principles of Financial Accounting (ACCT 2610) at Washington University in St. Louis will find this particularly helpful when learning to translate balance sheet and income statement data into a cash flow statement. It’s ideal for reinforcing concepts covered in lectures and during problem sets. This example can be used as a reference point when tackling your own cash flow statement exercises, helping you to visualize the relationships between different financial statement elements. It’s most beneficial *after* you’ve grasped the fundamental definitions and classifications of cash flow activities.

Common Limitations or Challenges

This example provides a single, specific illustration. It does not offer a comprehensive range of scenarios or industry-specific adaptations. It won’t walk you through the step-by-step process of *creating* a statement from scratch, nor does it cover advanced topics like the statement of cash flows for not-for-profit organizations. It’s intended to solidify understanding through observation, not to replace active problem-solving or a thorough review of course materials. Access to the full resource is required to understand the detailed calculations and reasoning behind the presented information.

What This Document Provides

* Comparative Balance Sheets for two periods (2003 & 2004)

* An Income Statement for the year ended December 31, 2004

* Illustrative T-Accounts related to key balance sheet accounts

* A complete Statement of Cash Flows prepared using the Direct Method

* A complete Statement of Cash Flows prepared using the Indirect Method

* A clear presentation of cash flows categorized into Operating, Investing, and Financing activities.