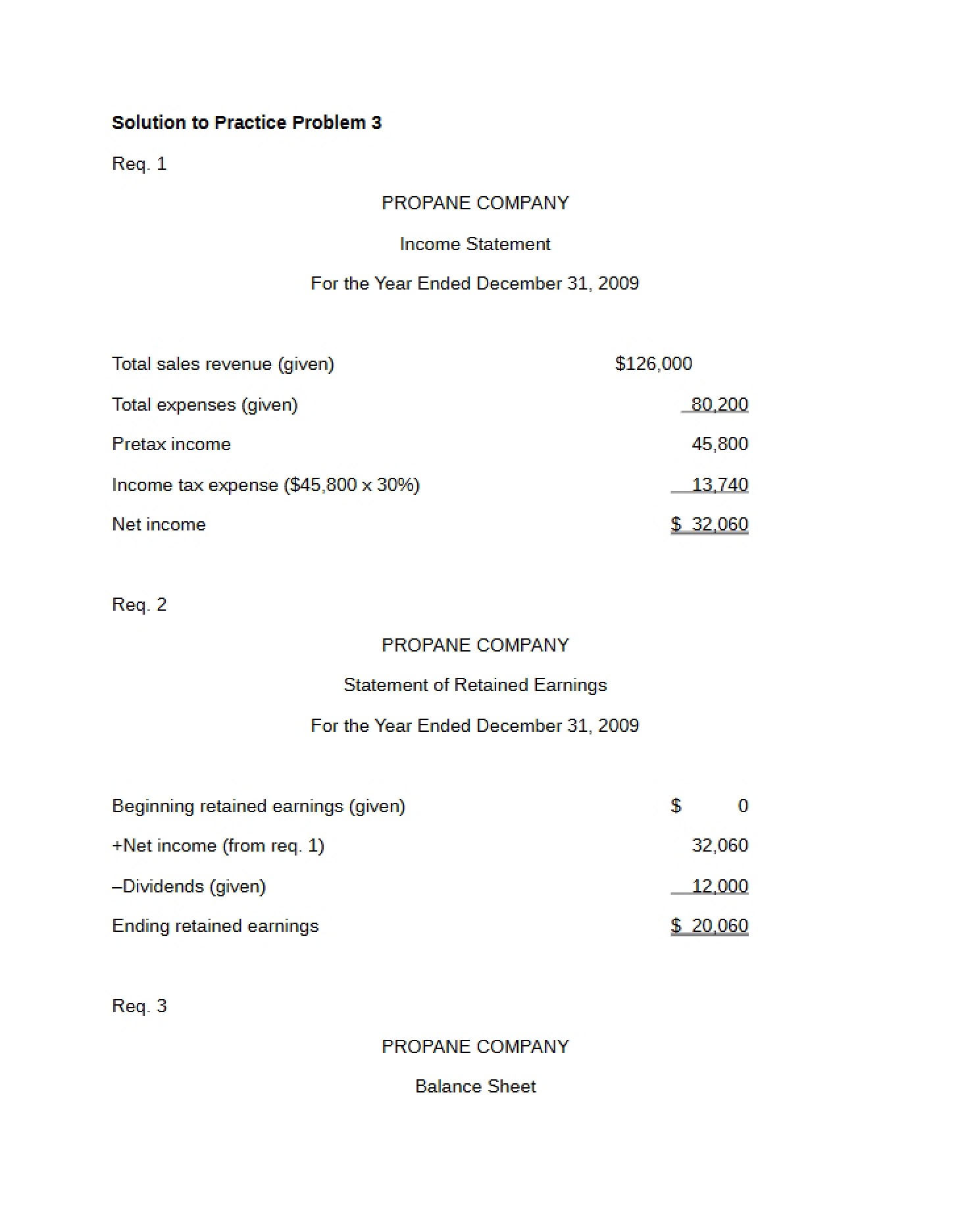

What This Document Is

This resource is a focused guide detailing the foundational mechanics of recording common business transactions. Specifically, it centers on the creation of journal entries – the initial step in the accounting cycle. It’s designed for students learning the core principles of financial accounting, covering key activities across the early stages of a business’s operational life. The material is organized by chapter, referencing concepts typically found in introductory financial accounting coursework.

Why This Document Matters

This guide is incredibly valuable for students in Principles of Financial Accounting (like ACCT 2610 at Washington University in St. Louis) who are building a strong understanding of debits and credits. It’s particularly helpful when you’re first learning to translate real-world business events into the language of accounting. Use this as a reference while working through homework assignments, preparing for quizzes, or reviewing before exams. It’s ideal for solidifying your understanding of *how* transactions impact the accounting equation. If you’re struggling to visualize the flow of financial information, this resource can provide clarity.

Common Limitations or Challenges

This guide focuses exclusively on the journal entry aspect of accounting. It does *not* cover the broader accounting cycle, including posting to ledgers, preparing trial balances, or creating financial statements. It also doesn’t delve into complex accounting scenarios or industry-specific transactions. The resource assumes a basic understanding of the accounting equation (Assets = Liabilities + Equity) and the fundamental accounting elements. It’s a building block, not a comprehensive solution.

What This Document Provides

* A structured overview of typical transactions encountered in the early stages of a business.

* Categorization of transactions based on common business activities.

* A framework for understanding the impact of transactions on key accounting elements.

* Organization of content aligned with typical introductory accounting chapters.

* A focus on the fundamental principles of debit and credit application.